|

Anglican Church of Southern African

|

| |||||

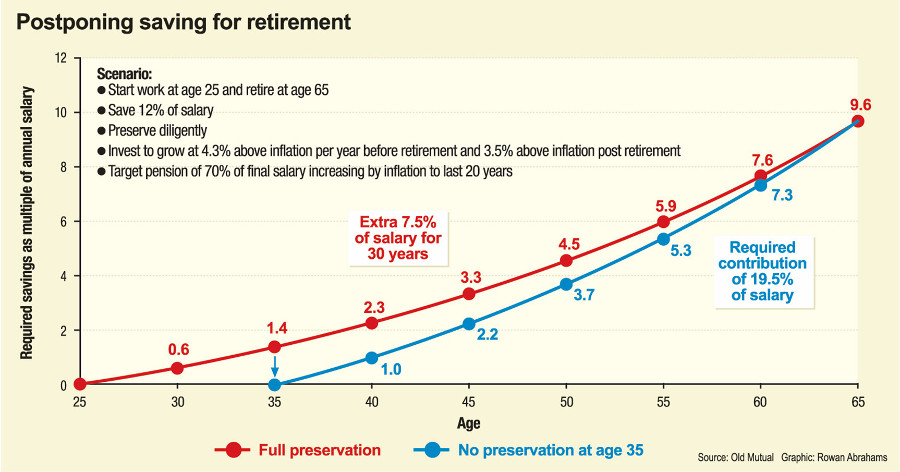

We acknowledge with grateful thanks both Personal Finance and Old Mutual Corporate Consultants for allowing this article to be used on the Anglican Church Pension Fund webpage. For many clergy and laity coming into the service of the church, it is seldom a first vocation that sees someone entering the church. All too often we have seen retirement savings from previous employers not brought into either of the pension funds offered by the church and as a result members of the pension funds are often 'short' of income on retirement. The value of preserving your retirement benefits from previous employment is highlighted in the article below. Will you really catch up by saving later? South African households are being forced to tighten their belts as the country sinks into a recession for the first time in eight years. You may be tempted to dip into your retirement savings, but the impact on your financial security could be devastating. The recently released 2017 Old Mutual Corporate Retirement Monitor shows there has been a dramatic increase (35% compared with 19% four years ago) in the number of fund members who intend to withdraw cash from their retirement savings if they change jobs. This behaviour is influenced by several factors, including the economic downturn, the higher level of debt, the increase in retrenchments, and the tendency to change jobs more frequently. The Retirement Monitor also found that, when changing jobs, fewer members (8% compared with 12%) are switching to a retirement annuity fund if their new employer does not provide a retirement fund or transferring their retirement savings to a preservation fund (3% compared with 6%). Fund members often fail to take account of the huge impact that accessing their retirement savings will have on their finances in the future. This may be because they have not been informed of this reality. The following example illustrates the point: at the age of 25, Joe Soap starts to contribute 12% of his salary to his retirement savings. If his savings earn, on average, a return of 4.3% above inflation a year, Joe will accumulate savings of almost 10 times his annual salary at retirement, assuming he works for 40 years. His accumulated savings (including interest) will be sufficient to provide a retirement income of about 70% of his final salary. If his savings continue to earn an after-inflation return of 3.5% a year after he retires, Joe could receive annual pension increases roughly in line with the inflation rate, and his retirement savings could last for 20 years, or until he turns 85. Changing jobs Let's say that Joe finds a new job when he is 35. At this stage, 30 years before he retires, Joe would have saved 1.4 times his annual salary. Two things are likely to influence what Joe decides to do with his savings:

Although it might seem that he still has enough time to catch up with his savings strategy, if Joe cashes out at when he is 35, the impact on his savings will be significant. If he cashes out, he will have reset his retirement savings to zero, but his retirement needs will not have changed. He still needs to accumulate 9.6 times his annual salary by the age of 65. To achieve this, Joe will have to contribute an additional 7.5% of his salary 'a total of 19.5% of his annual salary' towards his retirement savings. Most people cannot afford to contribute an additional 7.5% of their income to their retirement savings, and it is this 'recovery gap' that people tend to underestimate when they access their retirement savings relatively early in their working life. The graph below highlights the 'catch-up' required to make good on the postponement of retirement funding. If Joe cashes in his retirement savings at the age of 45, he will have to contribute 35% of his annual salary to catch up with his retirement savings goal. Furthermore, he will not be able to claim the entire contribution as a tax deduction, because the annual limit is 27.5% of the greater of remuneration or taxable income. The deduction has an annual cap of R350 000. The harsh reality is that, although you may justify accessing your retirement savings by saying that you will catch up, very few people can afford to put away a huge chunk of their income, least of all those whose financial situation is such that they have to access their savings in order to make ends meet. Tax penalties National Treasury has recognised the growing impact that the culture of 'dis-saving' is having on the economy. In addition to the heavy tax penalties for early withdrawals of retirement savings, Treasury is looking at other ways to dis-incentivise this behaviour. These measures include making it compulsory to preserve your retirement savings in all but a few extreme circumstances, such as severe illness or retrenchment. If you change jobs and withdraw a lump sum from your retirement savings, only the first R25 000 is tax-free. You are entitled to this R25 000 tax-free allowance only once before you retire. The next time you withdraw your retirement savings, you will pay tax on the full amount, starting at 18% for amounts between R25 001 and R660 000. The top rate is 36%. These punitive rates do not apply if you withdraw your savings only when you retire. | |

All content © Anglican Church of Southern African. All rights reserved.